The Bank for International Settlements

The Bank for International Settlements

Index | Homepage | Good Links | Bad Links | Search | Guestbook/Forum

The Bank for International Settlements

Unraveling the Basel Capital Accord

05Aug03 - Bank watching in Basel

05Aug03 - Bank watching in Basel

I was on business-travel from city to city in Switzerland. After the work in Basel I went straight to the BIS to see the buildings in real life.

In Basel, I noticed that there are two BIS-buildings, about a kilometer from eachother. The 'Botta'-building at the Aeschenplatz is a former UBS-bank. It has a door with the ABN-Amro-bank next door, very strange. ABN-Amro has a indoor connection with BIS, I saw it with my own two eyes!

After that I went to Geneva via Evian. Evian-les-Bains in France was also a place worth to visit.

I didn't dare to take pictures of some particular buildings, because through my remarkable behavior in Basel I was followed by Securitas people everywhere I went. There was no place in Switzerland where I had to introduce myself, because Securitas already knew me in advance.

Of course I have been at 'Place des Nations', where all the global organisations are based. Also I've been in the most-shattered bank in Geneva: the UBS-headquarters, it was full of nasty punchholes in the glass windows because of the quite recent demonstrations. Swiss people were really flabbergasted, because such demonstration of hooligans at the anti-globalists demonstrations are new to them.

Everywhere I went, I was protected by Securitas. 'Big Bro Securitas' was watching me all the time. I enjoyed every minute of it, because of the predictable manners of Securitas-employees. Also in Bern I was heavily protected by Securitas.

Back in Basel I went into the BIS building at the Central Station Place to try to open a bank-account. At that moment there was a press-conference going on, how strange. The Securitas-guy in front of the building recognized me, so he didn't ask a thing and let me go to do what I want to do. I asked the receptionist to open a bank account, but he lied to me that BIS is a private-bank.

After that I went to the Aeschenplatz and went in. The receptionist told me frankly that the B.I.S. "IS NOT A BANK". Thanks, lady receptionist, that was exactly what I wanted to hear, that BIS is not a bank. Now it is confirmed by this BIS-employee!

Ruling the World of Money

Ruling the World of Money

TEN TIMES A YEAR - once a month except in August and October - a small group of well dressed men arrives in Basel, Switzerland. Carrying overnight bags and attaché cases, they discreetly check into the Euler Hotel, across from the railroad station. They have come to this sleepy city from places as disparate as Tokyo, London, and Washington, D.C., for the regular meeting of the most exclusive, secretive, and powerful supranational club in the world.

Each of the dozen or so visiting members has his own office at the club, with secure telephone lines to his home country. The members are fully serviced by a permanent staff of about 300, including chauffeurs, chefs, guards, messengers, translators, stenographers, secretaries, and researchers. Also at their disposal are a brilliant research unit and an ultramodern computer, as well as a secluded country club with tennis courts and a swimming pool, a few kilometres outside of Basel.

The membership of this club is restricted to a handful of powerful men who determine daily the interest rate, the availability of credit, and the money supply of the banks in their own countries. They include the governors of the U.S. Federal Reserve, the Bank of England, the Bank of Japan, the Swiss National Bank, and the German Bundesbank. The club controls a bank with a $40 billion kitty in cash, government securities, and gold that constitutes about one tenth of the world's available foreign exchange. The profits earned just from renting out its hoard of gold (second only to that of Fort Knox in value) are more than sufficient to pay for the expenses of the entire organization. And the unabashed purpose of its elite monthly meetings is to coordinate and, if possible, to control all monetary activities in the industrialized world. The place where this club meets in Basel is a unique financial institution called the Bank for International Settlements - or more simply, and appropriately, the BIS (pronounced "biz" in German).

THE

BIS was originally established in May 1930 by bankers and diplomats of Europe

and the United States to collect and disburse Germany's World War I reparation

payments (hence its name). It was truly an extraordinary arrangement. Although

the BIS was organized as a commercial bank with publicly held shares, its

immunity from government interference - and taxes in both peace and war was

guaranteed by an international treaty signed in The Hague in 1930. Although

all its depositors are central banks, the BIS has made a profit on every

transaction. And because it has been highly profitable, it has required no

subsidy or aid from any government.

THE

BIS was originally established in May 1930 by bankers and diplomats of Europe

and the United States to collect and disburse Germany's World War I reparation

payments (hence its name). It was truly an extraordinary arrangement. Although

the BIS was organized as a commercial bank with publicly held shares, its

immunity from government interference - and taxes in both peace and war was

guaranteed by an international treaty signed in The Hague in 1930. Although

all its depositors are central banks, the BIS has made a profit on every

transaction. And because it has been highly profitable, it has required no

subsidy or aid from any government.

Since it also provided, in Basel, a safe and convenient repository for the gold holdings of the European central banks, it quickly evolved into the bank for central banks. As the world depression deepened in the Thirties and financial panics flared up in Austria, Hungary, Yugoslavia, and Germany, the governors in charge of the key central banks feared that the entire global financial system would collapse unless they could closely coordinate their rescue efforts. The obvious meeting spot for this desperately needed coordination was the BIS, where they regularly went anyway to arrange gold swaps and war-damage settlements.

Even though an isolationist Congress officially refused to allow the U.S. Federal Reserve to participate in the BIS, or to accept shares in it (which were instead held in trust by the First National City Bank), the chairman of the Fed quietly slipped over to Basel for important meetings. World monetary policy was evidently too important to leave to national politicians. During World War II, when the nations, if not their central banks, were belligerents, the BIS continued operating in Basel, though the monthly meetings were temporarily suspended. In 1944, following Czech accusations that the BIS was laundering gold that the Nazis had stolen from occupied Europe, the American government backed a resolution at the Bretton Woods Conference calling for the liquidation of the BIS. The naive idea was that the settlement and monetary-clearing functions it provided could be taken over by the new International Monetary Fund. What could not be replaced, however, was what existed behind the mask of an international clearing house: a supranational organization for setting and implementing global monetary strategy, which could not be accomplished by a democratic, United Nations-like international agency. The central bankers, not about to let their club be taken from them, quietly snuffed out the American resolution.

After World War II, the BIS reemerged as the main clearing house for European currencies and, behind the scenes, the favored meeting place of central bankers. When the dollar came under attack in the 1960s, massive swaps of money and gold were arranged at the BIS for the defence of the American currency. It was undeniably ironic that, as the president of the BIS observed, "the United States, which had wanted to kill the BIS, suddenly finds it indispensable." In any case, the Fed has become a leading member of the club, with either Chairman Paul Volcker or Governor Henry Wallich attending every "Basel weekend."

"It was in the wood-paneled rooms above the shop and the hotel that decisions were reached to devalue or defend currencies, to fix the price of gold, to regulate offshore banking, and to raise or lower short-term interest rates."

ORIGINALLY, the central bankers sought complete

anonymity for their activities. Their headquarters were in an abandoned

six-storey hotel, the Grand et Savoy Hotel Universe, with an annex above

the adjacent Frey's Chocolate Shop. There purposely was no sign over the

door identifying the BIS so visiting central bankers and gold dealers used

Frey's, which is across the street from the railroad station, as a convenient

landmark. It was in the wood-paneled rooms above the shop and the hotel that

decisions were reached to devalue or defend currencies, to fix the price

of gold, to regulate offshore banking, and to raise or lower short-term interest

rates. And though they shaped "a new world economic order" through these

deliberations (as Guido Carli, then the governor of the Italian central bank,

put it), the public, even in Basel, remained almost totally unaware of the

club and its activities.

ORIGINALLY, the central bankers sought complete

anonymity for their activities. Their headquarters were in an abandoned

six-storey hotel, the Grand et Savoy Hotel Universe, with an annex above

the adjacent Frey's Chocolate Shop. There purposely was no sign over the

door identifying the BIS so visiting central bankers and gold dealers used

Frey's, which is across the street from the railroad station, as a convenient

landmark. It was in the wood-paneled rooms above the shop and the hotel that

decisions were reached to devalue or defend currencies, to fix the price

of gold, to regulate offshore banking, and to raise or lower short-term interest

rates. And though they shaped "a new world economic order" through these

deliberations (as Guido Carli, then the governor of the Italian central bank,

put it), the public, even in Basel, remained almost totally unaware of the

club and its activities.

In May 1977, however, the BIS gave up its anonymity, against the better judgement of some of its members, in exchange for more efficient headquarters. The new building, an eighteen-story-high circular skyscraper that rises over the medieval city like some misplaced nuclear reactor, quickly became known as the "Tower of Basel" and began attracting attention from tourists. "That was the last thing we wanted, " Dr. Fritz Leutwiler, current president of both the BIS and the Swiss National Bank, explained to me while watching currency changes flash across the Reuters screen in his office. "If it had been up to me, it never would have been built."

Despite

its irksome visibility, the new headquarters does have the advantages of

luxurious space and Swiss efficiency. The building is completely air-conditioned

and self-contained, with its own nuclear-bomb shelter in the sub-basement,

a triply redundant fire-extinguishing system (so outside firemen never have

to be called in), a private hospital, and some twenty miles of subterranean

archives. "We try to provide a complete clubhouse for central bankers ...

a home away from home," said Gunther Schleiminger, the super-competent general

manager, as he arranged a rare tour of the headquarters for me.

Despite

its irksome visibility, the new headquarters does have the advantages of

luxurious space and Swiss efficiency. The building is completely air-conditioned

and self-contained, with its own nuclear-bomb shelter in the sub-basement,

a triply redundant fire-extinguishing system (so outside firemen never have

to be called in), a private hospital, and some twenty miles of subterranean

archives. "We try to provide a complete clubhouse for central bankers ...

a home away from home," said Gunther Schleiminger, the super-competent general

manager, as he arranged a rare tour of the headquarters for me.

The top floor, with a panoramic view of three countries - Germany, France, and Switzerland - is a deluxe restaurant, used only to serve the members a buffet dinner when they arrive on Sunday evenings to begin the "Basel weekends." Aside from those ten occasions, this floor remains ghostly empty.

On the floor below, Schleiminger and his small staff sit in spacious offices, administering the day-to-day details of the BIS and monitoring activities on lower floors as if they were running an out-of-season hotel.

The next three floors down are suites of offices reserved for the central bankers. All are decorated in three colors - beige, brown, and tan - and each has a similar modernistic lithograph over the desk. Each office also has coded speed-dial telephones that at a push of a button directly connect the club members to their offices in their central banks back home. The completely deserted corridors and empty offices - with nameplates on the doors and freshly sharpened pencils in cups and neat stacks of incoming papers on the desks - are again reminiscent of a ghost town. When the members arrive for their forthcoming meeting in November, there will be a remarkable transformation, according to Schleiminger, with multilingual receptionists and secretaries at every desk, and constant meetings and briefings.

On the lower floors are the BIS computer, which is directly linked to the computers of the member central banks, and provides instantaneous access to data about the global monetary situation, and the actual bank, where eighteen traders, mainly from England and Switzerland, continually roll over short-term loans on the Eurodollar markets and guard against foreign-exchange losses (by simultaneously selling the currency in which the loan is due). On yet another floor, gold traders are constantly on the telephone arranging loans of the bank's gold to international arbitragers, thus allowing central banks to make interest on gold deposits.

Occasionally there is an extraordinary situation, such as the decision to sell gold for the Soviet Union, which requires a decision from the "governors," as the BIS staff calls the central bankers. But most of the banking is routine, computerized, and riskless. Indeed, the BIS is prohibited by its statutes from making anything but short-term loans - most are for thirty days or less - that are government-guaranteed or backed with gold deposited at the BIS. The profits the BIS receives for essentially turning over the billions of dollars deposited by the central banks amounted to $162 million last year.

AS SKILLED as the BIS may be at all this, the central banks themselves have highly competent staff capable of investing their deposits. The German Bundesbank, for example, has a superb international trading department and 15,000 employees - at least twenty times as many as the BIS staff. Why then do the Bundesbank and the other central banks transfer some $40 billion of deposits to the BIS and thereby permit it to make such a profit?

One answer is, of course, secrecy. By commingling part of their reserves in what amounts to a gigantic mutual fund of short-term investments, the central banks create a convenient screen behind which they can hide their own deposits and withdrawals in financial centers around the world. For example, if the BIS places funds in Hungary, the individual central banks do not have to answer to their governments for investing in a communist country. And the central banks are apparently willing to pay a high fee to use the cloak of the BIS.

There is, however, a far more important reason why the central banks regularly transfer deposits to the BIS: they want to provide it with a large profit to support the other services it provides. Despite its name, the BIS is far more.than a bank. From the outside, it seems to be a small, technical organization. Just eighty-six of its 298 employees are ranked as professional staff. But the BIS is not a monolithic institution: artfully concealed within the shell of an international bank, like a series of Chinese boxes one inside another, are the real groups and services the central bankers need -- and pay to support.

The first box inside the bank is the board of directors, drawn from the eight European central banks (England, Switzerland, Germany, Italy, France, Belgium, Sweden, and the Netherlands), which meets on the Tuesday morning of each "Basel weekend." The board also meets twice a year in Basel with the central banks of Yugoslavia, Poland, Hungary, and other Eastern bloc nations. It provides a formal apparatus for dealing with European governments and international bureaucracies like the IMF or the European Economic Community (the Common Market). The board defines the rules and territories of the central banks with the goal of preventing governments from meddling in their purview. For example, a few years ago, when the Organization for Economic Cooperation and Development in Paris appointed a low-level committee to study the adequacy of bank reserves, the central bankers regarded it as poaching on their monetary turf and turned to the BIS board for assistance. The board then arranged for a high-level committee, under the head of Banking Supervision at the Bank of England, to preempt the issue. The OECD got the message and abandoned its effort.

To deal with the world at large, there is another Chinese box called the Group of Ten, or simply the "G-10." It actually has eleven full-time members, representing the eight European central banks, the U.S. Fed, the Bank of Canada, and the Bank of Japan. it also has one unofficial member: the governor of the Saudi Arabian Monetary Authority. This powerful group, which controls most of the transferable money in the world, meets for long sessions on the Monday afternoon of the "Basel weekend." It is here that broader policy issues, such as interest rates, money-supply growth, economic stimulation (or suppression) , and currency rates are discussed - if not always resolved.

Directly under the G-10, and catering to all its special needs, is a small unit called the "Monetary and Economic Development Department," which is, in effect, its private think tank. The head of this unit, the Belgian economist Alexandre Lamfalussy, sits in on all the G-10 meetings, then assigns the appropriate research and analysis to the half dozen economists on his staff. This unit also produces the occasional blue-bound "economic papers" that provide central bankers from Singapore to Rio de Janeiro, even though they are not BIS members, with a convenient party line. For example, a recent paper called "Rules versus Discretion: An Essay on Monetary Policy in an Inflationary Environment," politely defused the Milton Friedmanesque dogma and suggested a more pragmatic form of monetarism. And last May, just before the Williamsburg summit conference, the unit released a blue book on currency intervention by central banks that laid down the boundaries and circumstances for such actions. When there are internal disagreements, these blue books can express positions sharply contrary to those held by some BIS members, but generally they reflect a consensus of the G-10.

OVER A BRATWURST-AND-BEER lunch on the top floor of the Bundesbank, which is located in a huge concrete building (called "the bunker") outside of Frankfurt, Karl Otto Pöhl, its president and a ranking governor of the BIS, complained to me about the repetitiousness of the meetings during the "Basel weekend." "First there is the meeting on the Gold Pool, then, after lunch, the same faces show up at the G-10, and the next day there is the board [which excludes the U.S., Japan, and Canada], and the European Community meeting [which excludes Sweden and Switzerland from the previous group]." He concluded: "They are long and strenuous - and they are not where the real business gets done." This occurs, as Pöhl explained over our leisurely lunch, at still another level of the BIS: "a sort of inner club," as he put it.

The inner club is made up of the half dozen or so powerful central bankers who find themselves more or less in the same monetary boat: along with Pöhl are Volcker and Wallich from the Fed, Leutwiler from the Swiss National Bank, Lamberto Dini of the Bank of Italy, Haruo Mayekawa of the Bank of Japan, and the retired governor of the Bank of England, Lord Gordon Richardson (who had presided over the G -10 meetings for the past ten years). They are all comfortable speaking English; indeed, Pöhl recounted how he has found himself using English with Leutwiler, though both are of course native German-speakers. And they all speak the same language when it comes to governments, having shared similar experiences. Pöhl and Volcker were both undersecretaries of their respective treasuries; they worked closely with each other, and with Lord Richardson, in the futile attempts to defend the dollar and the pound in the 1960s. Dini was at the IMF in Washington, dealing with many of the same problems. Pöhl had worked closely with Leutwiler in neighboring Switzerland for two decades. "Some of us are very old friends," Pöhl said. Far more important, these men all share the same set of well-articulated values about money.

The prime value, which also seems to demarcate the inner club from the rest of the BIS members, is the firm belief that central banks should act independently of their home governments. This is an easy position for Leutwiler to hold, since the Swiss National Bank is privately owned (the only central bank that is not government owned) and completely autonomous. ("I don't think many people know the name of the president of Switzerland - even in Switzerland," Pöhl joked, "but everyone in Europe has heard of Leutwiler.") Almost as independent is the Bundesbank; as its president, Pöhl is not required to consult with government officials or to answer the questions of Parliament - even about such critical issues as raising interest rates. He even refuses to fly to Basel in a government plane, preferring instead to drive in his Mercedes limousine.

The Fed is only a shade less independent than the Bundesbank: Volcker is expected to make periodic visits to Congress and at least to take calls from the White House - but he need not follow their counsel. While in theory the Bank of Italy is under government control, in practice it is an elite institution that acts autonomously and often resists the government. (In 1979, its then governor, Paolo Baffi, was threatened with arrest, but the inner club, using unofficial channels, rallied to his support.) Although the exact relationship between the Bank of Japan and the Japanese government purposely remains inscrutable, even to the BIS governors, its chairman, Mayekawa, at least espouses the principle of autonomy. Finally, though the Bank of England is under the thumb of the British government, Lord Richardson was accepted by the inner club because of his personal adherence to this defining principle. But his successor, Robin Leigh-Pemberton, lacking the years of business and personal contact, probably won't be admitted to the inner circle.

In any case, the line is drawn at the Bank of England. The Bank of France is seen as a puppet of the French government; to a lesser degree, the remaining European banks are also perceived by the inner club as extensions of their respective governments, and thus remain on the outside.

A second and closely related belief of the inner club is that politicians should not be trusted to decide the fate of the international monetary system. When Leutwiler became president of the BIS in 1982, he insisted that no government official be allowed to visit during a "Basel weekend." He recalled that in 1968, U.S. Treasury undersecretary Fred Deming had been in Basel and stopped in at the bank. "When word got around that an American Treasury official was at the BIS," Leutwiler said, "bullion traders, speculating that the U.S. was about to sell its gold, began a panic in the market." Except for the annual meeting in June (called " the Jamboree" by the staff), when the ground floor of the BIS headquarters is open to official visitors, Leutwiler has tried to enforce his rule strictly. "To be frank," he told me, "I have no use for politicians. They lack the judgement of central bankers." This effectively sums up the common antipathy of the inner club toward "government muddling," as Pöhl puts it.

The inner-club members also share a strong preference for pragmatism and flexibility over any ideology, whether that of Lord Keynes or Milton Friedman. For this reason, there was considerable apprehension last spring that Paul Volcker would be replaced by a supply-side ideologue like Beryl Sprinkel, and considerable relief when he was reappointed for another term. Rather than resorting to rhetoric and invoking principles, the inner club seeks any remedy that will relieve a crisis. For example, earlier this year, when Brazil failed to pay back on time a BIS loan that was guaranteed by the central banks, the inner club quietly decided to extend the deadline instead of collecting the money from guarantors. "We are constantly engaged in a balancing act - without a safety net," Leutwiler explained.

THE FINAL AND by far the most important belief of the inner club is the conviction that when the bell tolls for any single central bank it tolls for them all. When Mexico faced bankruptcy last year, for instance, the issue for the inner club was not the welfare of that country but, as Dini put it, "the stability of the entire banking system." For months Mexico had been borrowing overnight funds from the interbank market in New York - as every bank recognized by the Fed is permitted to do - to pay the interest on its $80 billion external debt. Each night it had to borrow more money to repay the interest on the previous nights transactions, and, according to Dini, by August Mexico had borrowed nearly one quarter of all the "Fed Funds," as these overnight loans between banks are called.

The Fed was caught in a dilemma: if it suddenly stepped in and forbade Mexico from further using the interbank market, Mexico would be unable to repay its enormous debt the next day, and 25 percent of the entire banking system's ready funds might be frozen. But if the Fed permitted Mexico to continue borrowing in New York, in a matter of months it would suck in most of the interbank funds, forcing the Fed to expand drastically the supply of money.

It was clearly an emergency for the inner club. After speaking to Miguel Mancera, director of the Banco de Mexico, Volcker immediately called Leutwiler, who was vacationing in the Swiss mountain village of Grison. Leutwiler realized that the entire system was confronted by a financial time bomb: even though the IMF was prepared to extend $4.5 billion to Mexico to relieve the pressure on its long-term debt, it would require months of paperwork to get approval for the loan. And Mexico needed an immediate fix of $1.85 billion to get out of the interbank market, which Mancera had agreed to do. But in less than forty-eight hours, Leutwiler had called the members of the inner club and arranged the temporary bridging loan.

While this $1.85 billion appeared - at least in the financial press - to have come from the BIS, virtually all the funds came from the central banks in the inner club. Half came directly from the United States - $600 million from the Treasury's exchange-equalization fund and $325 million from the Fed's coffers; the remaining $925 million mainly from the deposits of the Bundesbank, Swiss National Bank, Bank of England, Bank of Italy, and Bank of Japan, deposits that were specifically guaranteed by these central banks, though advanced pro forma by the BIS (with a token amount advanced by the BIS itself against the collateral of Mexican gold). The BIS undertook virtually no risk in this rescue operation; it merely provided a convenient cloak for the inner club. Otherwise, its members, especially Volcker, would have had to take the political heat individually for what appeared to be the rescue of an underdeveloped country. In fact, they were - true to their paramount values - rescuing the banking system itself.

On August 31 of this year, Mexico repaid the BIS loan. But the bailout was only a temporary, if not pyrrhic, victory. With the multibillion-dollar debts of a score of other countries - including Argentina, Chile, Venezuela, Brazil, Zaire, the Philippines, Poland, Yugoslavia, Hungary, and even Israel - hanging like so many swords of Damocles over its sacred monetary system, the inner club has "no choice," as Leutwiler has concluded, but to remain a crisis manager. This new role has created considerable concern among the outer circle, and even in the Bank of England, since the members who don't entirely share the mentality of the inner club want the BIS to remain primarily a European institution. "Let the Fed worry about Brazil and the rest of Latin America - that is not the job of the BIS," a blunt representative of the Bank of England, definitely not part of the inner club, told me. Others at the BIS have argued that it does not have the experience or facilities to become "a mini-IMF - putting out fires around the world," as one staffer described it.

To mollify such dissent on the periphery, inner club members publicly pay lip service to the ideal of preserving the character of the BIS and not turning it into a lender of last resort for the world at large. Privately, however, they will undoubtedly continue their maneuvers to protect the banking system at whatever point in the world it seems most vulnerable. After all, it is ultimately the central banks' money at risk, not the BIS's. And the inner club will also keep using the BIS as its public mask - and pay the requisite price for the disguise.

The next meeting of the inner club is Monday, November 7.....

Edward Jay Epstein is the author of The Rise and Fall of Diamonds, Legend: The Secret World of Lee Harvey Oswald, and News From Nowhere. He also has written a book on international deception.

Investor's Business Daily, May 1, 1992 summed up the character of the BIS in an article entitled:

Why a Global Credit Crunch? Some say Little-known BIS Is Partly to Blame - Despite its global anonymity, the BIS is one of the most powerful financial institutions in the world ...

In the book Global Financial Integration: the End of Geography, author Richard F. O'Brien further confirms the powerful role of the BIS:

In the financial marketplace, the trend towards some sort of global governance is best represented by the efforts of bank supervisors under the aegis of the Bank for International Settlements in Basel to impose common minimum capital requirements on banks ... and to integrate and coordinate the supervision of banking, securities markets and insurance ...

Financial World Magazine - February 16, 1993 "Where Has All the Money Gone?" explains how the BIS has more recently flexed its muscle:

Even before Japan's equity markets began to contract, regulations put into effect in 1988 by the Bank of International Settlement's Committee on Banking regulation and Supervisory Practices had begun to exact a particularly heavy toll on Japanese lenders. Those regulations require the world's bankers to raise their underlying asset bases, the money against which they lend, to 8% to total capital, more than double the asset average of the 1980's.- J Epstein

Carrol

Quigley - the bankers' plan

Carrol

Quigley - the bankers' plan

"The Power of financial capitalism had [a] far reaching plan, nothing less than to create a world system of financial control in private hands able to dominate the political system of each country and the economy of the world as a whole.This system was to be controlled in a feudalistic fashion by the central banks of the world acting in concert, by secret agreements arrived at in frequent meetings and conferences.

The apex of the system was to be the Bank for International Settlements in Basel, Switzerland, a private bank owned and controlled by the world's central banks, which were themselves private corporations.

Each central bank sought to dominate its government by its ability to control treasury loans, to manipulate foreign exchanges, to influence the level of economic activity in the country, and to influence co-operative politicians by subsequent rewards in the business world."

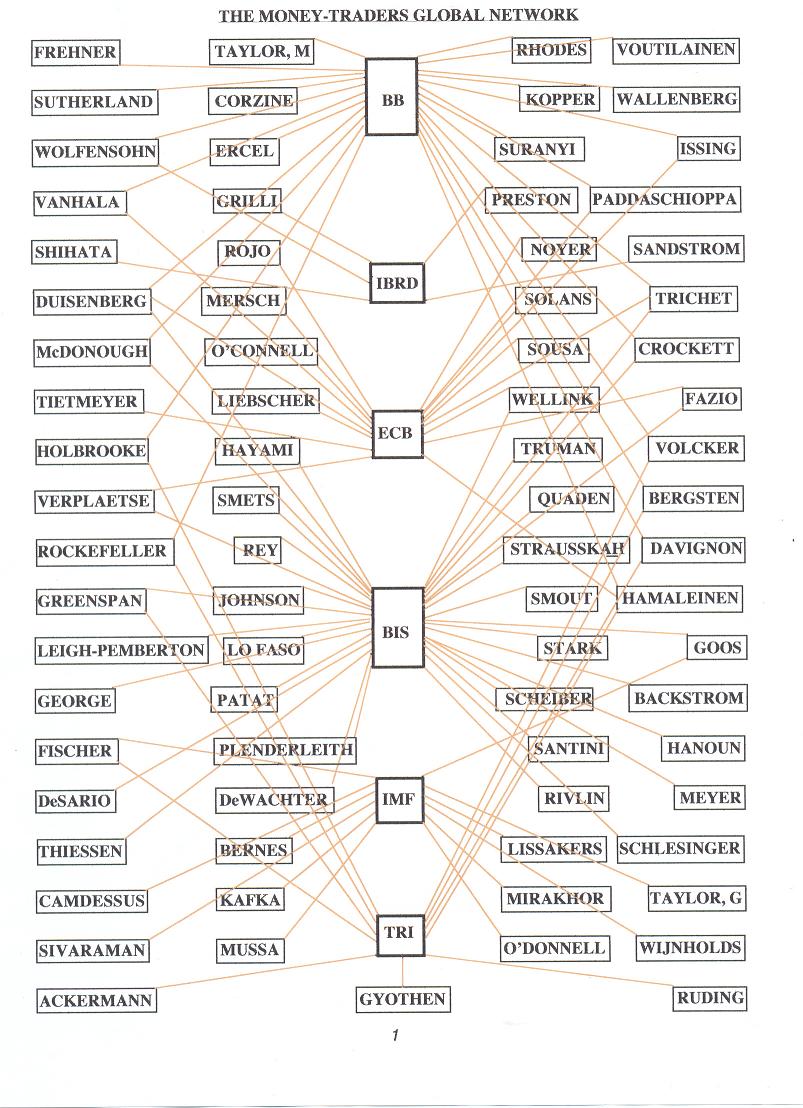

THE NETWORK

THE NETWORK

See

also Alfred Mendez' article AN UNCOMMON VIEW

OF THE BIRTH OF AN UNCOMMON MARKET on my Bilderberg History page

See

also Alfred Mendez' article AN UNCOMMON VIEW

OF THE BIRTH OF AN UNCOMMON MARKET on my Bilderberg History page

The wealth of the country flees the land

Like cottonseed on a wind

Blown by the fetid breath

Of money-pimps in Bedlam

Pursuing the creed of masters

Who worship a market freed

Of all restraints on greed -

While politicians posture

And feed on delusions of power

The above graph [couldn't reproduce it here, see below ed.] was created in order to bestow meaning in simplistic, delineated form to such terms as 'free market', 'new world order' and 'globalisation' - terms that have dominated political/economic terminology over the past two decades-or-so, and the fact that it focusses on banks and bankers (a profession endowed with the aura of authority in the eyes of the public) is quite simply because, without money, those terms are meaningless. Indeed, the title itself emphasises the role of money: After all, what is a banker if he's not a trader in money? Similarly, 'globalisation' would be equally meaningless if such politically omnipotent groups as the Bilderberg Group and the Trilateral Commission were not taken into account when assessing it's (globalisation's) significance. Moreover, how is it possible to disassociate banker from politician from businessman when, at times, one individual is all three - and, in any case, they are constituent parts of a single entity: the corporate establishment? Hence the inclusion of these two groups withinthe graph.

The Bilderberg (or BB from now on) was formed in 1954 out of the need of corporate America to ensure cohesion of purpose on the part of its European partners in the recently formed North Atlantic Alliance (NATO) - the twin aim being to facilitate the flow of American capital into the region, and to bring Germany into the Alliance (against, it should be noted, the wishes of many of its partners). That it is a group endowed with enormous political clout can be attested to by: (1) examination of the lists of committee members and conference attendees over the years - together with the gravity and importance of the subjects discussed at these conferences (NATO, understandably, being repeatedly a key subject); and (2) these conferences take place under very strict security cover supplied by the respective host countries - even though implicit within the structure of this cabal is its unaccountable, secretive nature.

The Trilateral Commission (or TRI from now on) was formed in 1973, its agenda determined by the corporate-funded Brookings Institute and the Kettering Foundation - with not-a-little-help from David Rockefeller of the Chase/Manhattan Bank. That its projected formation should have been so enthusiastically acclaimed by the BB Conference in Knokke (Belgium) in 1972 should cause no surprise. Both corporate-controlled organisations, with linked membership, they shared the same aim: increasing globalisation of their wealth and power. Certainly, the BB with its total lack of any 'democratic accountability', must be in agreement with the TRI's declaration (published in their "The crisis of Democracy") that what the West needs most "is a greater degree of moderation in democracy". Though, on second thoughts, the former probably thinks the 'the degree of moderation' somewht understated!

A further examination of both graph and list of bankers' names reveals that, of the banking organisations, the Banks for International Settlements (or BIS from now on) is self-evidently of prime importance on the international scene - not only because of its prestigious membership (embracing as it does the head bankers of the leading industrial nations) - but also because of the significance of its links with other groups. This article will focus on it, at the expense of the other better-known banking institutions, for two reasons: (1) its prime ranking in the international hierarchy; and (2) so little knowledge of it is in the public domain.

The BIS is the world's oldest international financial institution, having been set up in 1930 with the twin aim of (1) coping with reparations/loans from/to a very unstable post-World War one Germany; and (2) more importantly, to act as a forum for central bankers in the future. As such, it was the epitome of supranationality - able to circumvent all those orthodox ideals that had, over the years, become synonymous with the concept of the 'nation state' - such as 'love of country', 'patriotism' etc., - the danger, of course, being that, in certain circumstances (such as a state of war), such circumvention of patriotism by any of its board members could lead to them being accused of treasonable offences.

In order to appreciate what followed, it is essential to offer a brief resumé of the political/economic situation at the turn of the century: the Industrial Revolution, having fostered the rapid growth of a capitalist economy, inevitably gave birth to an ideal/dogma exposing the socio-political discord inherent within that same system which was based on the concept of one comparatively small group of people garnering profit from the wealth created by the labor of a much larger group. Thus was Marxism born - leading to the Bolshevik revolution in 1917.The USSR, now perceived by the industrial nations as representing the very antithesis of capitalism, was henceforth 'the enemy'. The 'cold war' had begun, and its most blatant expression was the birth of fascism in the aftermath of the Bolshevik revolution - a birth both induced and nurtured by corporations such as I.G.Farben, SKF, Ford, ITT and Du Pont - corporation which were fast becoming multi-national in nature..Enter BIS. Set up in 1930 (see above),it consisted, initially, of a group of 6 central banks and a 'financial institution of the USA'. Granted a constitution charter by Switzerland, it was henceforth based in that country. That America was by then a financial force to be reckoned with on the international scene is borne out by the fact that the first President appointed to the BIS was Gates W. McGarrah (ex-Chase National Bank & Federal Reserve Bank).

By the late 1930's the BIS had assumed an openly pro-Nazi bias - much of it disclosed by Charles Higham in his book "Trading With the Enemy", and years later corroborated by a BBC Timewatch film "Banking With Hitler" (broadcast in late '98). Two examples of such bias (there were many more) were: (1) The BIS had arranged transfers into the account of the German's Reichbank of $378 million of what was, in effect, gold looted from the coffers of the invaded countries of Austria, Czechoslovakia, Holland and Belgium; and (2) in the summer of 1942, plans for the projected American invasion of Algeria were leaked to the governor of the French National Bank, who immediately contacted his German colleague in the BIS, SS Gruppenfuehrer Baron Kurt von Schroder (of the Stein Bank of Cologne), and by transferring 9 billion gold francs to Algiers - via the BIS - the Germans and their French subsidiaries made a killing of some $175 million in this dollar-exchange scam. Given the membership of the BIS at that time, this was hardly surprising. On the board were the following high-profile representatives of the Axis powers (there were 4 others): Walther Funk (Pres. of the Reichbank); Kurt von Schroder (above); Dr. Hermann Schmitz (Jt.Chm. of I.G.Farben); Emil Puhl (V/Pres. of the Reichbank); Yoneji Yamamoto; and Dr. V. Azzolini (Gov. Bank of Italy). It should be added that, of the non-Axis members on the board, many - such as Montagu Norman (Gov. of the Bank of England) were Nazi sympathisers, and that the President of the BIS from 1939 to 1946 was Thomas McKittrick, an American corporate lawyer who had been both Director of Lee, Higginson & Co. (a company which had made substantial loans to the Third Reich) and Chairman of the British-American Chamber of Commerce in London. His continued presidency of the BIS after America's entry into the war in December1941 was approved by Germany and Italy with this significant addendum to their note of authorisation: "McKittrick's opinions are safely known to us".

With the above noted disclosures in mind, the policy of appeasement pursued by Britain and France towards Germany in the pre-war period can now be more readily understood. By concluding a pact with Hitler, Britain and France - in effect - gave him the green light to advance eastwards (ref. "Mein Kampf"). Furthermore, the fact that they shared his endemic anti-communism blinded them to the risk that they were running by negotiating from a position of comparative military weakness - of which Hitler was perfectly aware - and for which they paid a heavy price. It should also be added that the architect of this act of appeasement, Prime Minister Chamberlain, was a shareholder in ICI, which had ties with I.G.Farben.

In the late '30's, and more particularly during World War 2, given America's great wealth - as opposed to Europe's straitened circumstances - it was inevitable that the trade between the two would be of a one-way nature, from the former to the latter. And not surprisingly, in view of the close relationship between American and German corporations (as noted above), a substantial portion of supplies went to Germany - often via fascist Spain - by ship and tanker under flags of neutrality. Many of the financial arrangements covering such trade were handled by BIS in neutral Basle. As an example of how substantial this trade was: in mid-'44 Am,erica was supplying Germany with 48 thousand tons of oil, and 11 hundred tons of much-needed wolfram (tungsten) per month! The fact that this trade was illegal in the USA for much of this period - and particularly after America's entry into the war in December '41 - did little to stop such trade. The large corporations, such as Standard Oil and ITT, saw to that. After all, then - as now - the US Administration was effectively under corporate control (as it has been since 1933, during FDR's term of office). Even the Secretary of Treasury, Henry Morgenthau, and his Assistant, Harry Dexter White, aware as they well were of the part played by BIS in this, could do little about it. In July '44, 730 delegates from 44 countries met at Bretton Woods to plan a framework for post-war international trade, payments and investments - a conference which subsequently resulted in the setting up in'47 of both the International Bank for Reconstruction & Development (IBRD, or World Bank) and the International Monetary Fund (IMF). The apparent inviolability of the BIS referred to above was perhaps best illustrated by the fact that Resolution 5, calling for the dissolution of BIS, was subsequently ignored and proven ineffective. The corporate establishment had seen to that - as indeed, it had seen to all such previous attempts.

With war's end now calling for a clearing of conscience, BIS's method of achieving this was by stressing its somewhat euphemistic neutrality, while playing down its less palatable, but quintessential supranationality. Their annual report of 1946 - as quoted in the Times - stated: "It is noted that the Bank has continued to supply the principles of strict neutrality, but that circumstances have caused a further decline in the volume of its business". Further: "Wars are the worst cause of monetary convulsions, and the first condition for enjoying the benefits of an ordinary monetary system is to establish and maintain a reign of peace". In view of their recent previous history, the term 'irony' hardly does justice to the above statements!. This report was, incidentally, the last to be signed by its President, Thomas McKittrick: in June 1946 he was appointedVice/Chairman of the Chase National Bank by its owners, the Rockefellers - presumably as a mark of gratitude for the assistance rendered to them by the BIS during his presidency.

In view of the somewhat puzzling fact that this now meant that there were in this post-war period three international financial/banking institutions - all with the self-evidently similar aim of resolving the world's serious economic problems - a brief, close look is called for in order to clarify the situation. The first (and intriguing) fact to be noted here is that, whereas the IMF and The World Bank have been frequently and conspicuously in the public eye from birth, the BIS has adopted a low profile and remained uncommunicative. This was an expedient tactic for the latter to adopt - for two reasons: (1) it thus eluded any investigation into its previous financial dealings with the Third Reich; and (2) more importantly, by so diassociating itself from the IMF and World Bank, the latter would henceforth be widely (though erroneously) regarded as the sole guardians of the worldwide economy, thus allowing the BIS more latitude to follow the agenda set by the corporate establishment - to whom, it must be recalled, they owed their survival.

This ambivalent relationship between the IMF/World Bank vis-a-vis the BIS/commercial banks in the 70's is epitomised by Anthony Sampson in his book "The Money Lenders": "The commercial banks in the meantime had created a very different perspective, for the IMF now controlled much less of the world's money. In 1966, the quotas which made up its capital amounted to 10% of the total world imports; but by '76 they made up only 4%"..."by '76 world annual deficits had reached $75 billion : of this, 7% financed by the IMF; 18% by other official international bodies (governments and World Bank) - remaining three-quarters financed by banks (commercial)". (Today, some two-and-a-half decades later, the board members of BIS, between them, control 95% of the money in circulation). The reason for this apparent taking over of such responsibility by the BIS from the IMF/World Bank is twofold: (1) the collapse of the Bretton Woods system of exchange convertibility in the early seventies exposed the irrelevance of the latter as agents for European reconstruction; and (2) the latter being statutorily-appointed agents of the UN, were therefore - ostensibly - accountable to a much wider constituency than the BIS, and therefore politically less manageable by the corporate establishment, whose primary aim in the aftermath of World War 2 was to ensure the unrestricted flow of American capital into Europe. A flow considerably eased by subsequent European integration, in which both NATO and the Bilderberg played a crucial role. This aim was furthered by means of the US Congressionally-authorised European Cooperation Act (ECA) of 1948, and implemented by its subsidiary, the European Payments Union (EPU) of 1950 - both under the aegis of the Marshall Plan of 1947. Predictably, the BIS was the institution chosen by the EPU to oversee this movement of capital (a point worthy of note here is that the head of the EPU at that time was one Richard Bissell, an economist who, years later, was to be the CIA Deputy Director of Planning overseeing the Bay of Pigs fiasco in April '61!).The BIS was now firmly ensconced in the heart of European integration, and was subsequently to play a critical role in the events leading to its (Europe's) eventual evolvement into the European Union, a bureaucratic politico-economic body occupying a position of crucial importance within the wider global hierarchy envisaged by the corporate establishment.

The significance of the American's key central role in this sequence of events is underscored by the fact that, in the aftermath of World War 2, they (the Americans) set up the Bundesbank in Frankfurt (in their zone of control), ensuring that the bank would be independent of government and follow a strict monetary policy - in effect, another Federal Reserve System. In 1948 they replaced the existing Reichmarks with approximately 11 billion Deutschmarks, and Germany's subsequent conduct vis-a-vis European integration must be viewed with this in mind. In any case, the fact remains that Germany's subsequent frequent delaying tactics enabled the dollar to consolidate its dominance.

In their published précis entitled "Profile of an International Organisation", the BIS states that its "predominant tasks are summed up most succintly in part of Article 3 of its original Statutes. They are 'to promote the co-operation of central banks and to provide additional facilities for international financial operations'". To achieve this aim it has 3 administrative bodies: (1) a Board of Directors, comprising the Governors of the central banks of Belgium, France, Germany, Italy, the UK and the USA, each of whom appoints another member of the same nationality - plus the central bank Governors of Canada, Japan,Holland, Sweden and Switzerland: a total of 17. (2) A Management Board; and (3) An annual General Meeting in June of each year.

That this is an organisation carrying enormous clout is readily confirmed by a closer look at said synopsis, pertinent quotes from which follow (italics are BIS's):

(A) "Since September 1994, the eleven countries from which the members of the Bank's Board of Directors are drawn have been identical with the countries which comprise the Group of Ten (G-10), with which the BIS has had a long and close association".

(B) "As well as making resources available to the IMF under the GAB (General Arrangements to Borrow) the G-10 has, since 1963, been a principal forum for discussion of international monetary questions. From the outset, the BIS has been a participant in G-10 Meetings, above all because the Governors of the G-10 central banks meet regularly on the occasion of the Basle monthly meetings. The G-10 meetings have, over time, become the pivotal forum in which much wider activities have been set in motion by the G-10 central banks in the pursuit of financial stability". (Meetings, it should be noted, hosted by the BIS in their high-rise office block in Basle).

(C) "As early as 1971 concern among central banks about the evolution of the Eurocurrency markets led to the establishment of a Standing Committee of the Group of Ten central banks which has met periodically in Basle ever since"

(D) In December 1994 the G-10 Governors set up "The Basle Committee on Banking Supervision, the secretariat for which is provided by the BIS".

(E) "The BIS hosts meeting of, and provides the secretariat for, the Committee on Payment and Settlement Systems and its various working parties".

(F) "..the BIS in a joint initiative with the Basle Committee on Banking Supervision is establishing an Institute for Financial Stability ahich is expected to commence its activities sometime in the second half of this year" (1998).

(G) " From 1964 until the end of 1993 the BIS hosted the Secretariat of the Committee of Governors of the Central Banks of the Member States of the European Economic Community (theCommittee of Governors). From 1st of June 1973 until the end of 1993 the Secretariat of the Committee of Governors also served the Board of Governors of the European Monetary Co-operation Fund (EMCF) and the Bank (BIS) acted as EMCF agent. Until they were replaced by the European Monetary Institute on 1st January 1994, the Committee of Governors and the EMCF were the Community bodies which provided the institutional framework for monetary co-operation in the European Community".

(It should be added that the above quotes are by no means a comprehensive listing in the synopsis of the BIS's activities on the global scene).

Three news items concerning the role played by the BIS are worthy of note:

(1) In 1994 the Belgian banker, Baron Alexandre Lamfalussy resigned from his post as General Manager of the BIS in order to become Head of the European Monetary Institute (EMI) - forerunner of the European Central Bank (ECB). As reported in the Times of 10/11/'93: Andrew Crockett (Executive Director of the Bank of England), who was replacing Lamfalussy as General Manager of the BIS,.."said he did not foresee the ENI..impinging on the work of the Basle-based BIS which is widely regarded as the central banker's central bank"..and adding that.."The EMI would enable the BIS to re-focus on global issues, and develop its role as a forum for collaboration between central banks in the monetary and regulatory fields".

(2) C.Fred Bergsten, Head of the Institute for International Economics, told the Washington Post on the 3rd of January '99 "The adoption of a common currency is by far the boldest chapter of European integration. Money traditionally has been an integral element of national sovereignty"..and the decision by Germany and France to give up their mark and franc "..represents the most dramatic voluntary surrender of sovereignty in recorded history. The European Central Bank that will manage the euro is a truly supranational institution".

(3) In the Independent On Sunday of the 21st February '99 it was reported that Andrew Crockett (see above) has been appointed Chairman of a newly-established 'Stability Forum' (see quote 'F' above), whose aim is to monitor global markets (this was the idea of Hans Tietmeyer, President of the Bundesbank).

Certain conclusions can be drawn from a recapitulation of the facts noted above:

(1) The BIS occupies a central role within the global/European financial scene - to the extent that such institutions as the G-10 and ECB (among others) play a surrogate role.

(2) The goal of the corporations is precisely the same today as it was at the end of the Great War. This is inevitable, inasmuch as inherent within the capitalist system is its obligation to the aggrandisement of profit.

(3) As a consequence, sovereignty - in the sense of a country's or organisation's political independence - can be ignored and overridden. This is happening today. The signs are there for all to see: Is America really in the Gulf Region for the benefit of its inhabitants ('ragheads' in American parlance)? Ask any oilman.

Are the two terms 'NATO' and the "International Community' really synonymous? Ask any country not in the Alliance.

Is the 'Cold War' really dead? Ask NATO why it is still in existence.

Is it not clear that NATO's primary role in Europe is to act as corporate America's anti-Marxist enforcer (even though the Marxism in question may be of a purely nominal nature)? Ask the head formulator of NATO, George Kennan (he may be dead, but his disclosure of the real reason for NATO's birth is on record in the BBC's Lord Reith Lecture of 1957).

Has not the UN's sovereignty been by-passed time-and-time again over the years? Ask its main debtor - America.

And finally, why is so little of the BIS in the public domain? Ask the owners/controllers of the means of communication - the media.

DAVIES, Glyn "A History of Money" (University of Wales '94)

DEDMAN, Martin "The Origins & Development of the European Union - '45 to '95 (Routledge '96)

HIGHAM, Charles "Trading With The Enemy" (Robert Hale '83)

MARSHALL, Matt "The Bank" (Random House '99)

SAMPSON, Anthony "The Money Lenders" (Hodder & Stoughton '81)

BIS Précis '98

INTERNET (Membership lists, etc.)

The "big five" prime banks of Wall Street, the owners of the "Class A" stock of the NewYork Federal Reserve Bank, are: Chase-Manhattan, Citibank, Guaranty Trust, Chemical/Manufacturers-Hannover, and Bankers' Trust. The Class A stock of the Federal Reserve has not been sold or traded on the open market since it was hermetically sealed from the public at the end of the summer of 1914. It is the exclusive property of Wall Street and European prime banks, whose major stockholders are the trans-Atlantic Ruling Class. This pattern holds true of Central Banks throughout the nations of the advanced capitalist sector. The Big Five have interlocking directorates with the "Seven Sisters," the Anglo-Dutch-American oil cartels: Exxon, BP (British Petroleum), Dutch-Royal Shell, Texaco, Mobil, Gulf, and Standard Oil of California (SOCAL).

Several of these trans-Atlantic money and commodity cartels financed Mussolini and Hitler and actively maintained their connections with the Reich throughout World War II. They were also all actively involved in Stalin's Russia by the beginning of the first Five Year Plan in 1928. None of this is really secret-anyone can discover the facts by doing a little research. Nor should it be considered a "conspiracy" (either by those who promote or deny the essential facts of the matter) - bankers and businessmen have been "trading with the enemy" for centuries. It is just one more example of "the wise investment policy" of cartels like J.P. Morgan and Co. and Standard Oil of New Jersey.

The seat of first world finance capital is Basel, Switzerland, where the Central Banks of the Group of Seven (G-7) form the directorate of the Bank for International Settlements (BIS). The G-7 include Britain, France, Germany, Italy, Canada, the U.S., and Japan. The G-7 are called the "Hard Currency Countries" because their Central banks, corporations privately owned by the Prime Banks of these nations, have acquired most of the mined, milled, and ingotted gold of the world. Approximately 80 percent of this is in the vaults of Credit Suisse, under the Berghoff, the airport in Zurich. A somewhat larger formation, called the G-10, includes Belgium, Holland, and Sweden.

The U.S. has become the greatest debtor nation on earth because the Prime Banks of the other nations of the G-10 (especially Britain, Holland, and Japan) have purchased the U.S. government debt in the form of semi-annual and tax-exempt U.S. Treasury Securities through the operations of the Federal Open Market Committee, the Fed's window on Wall Street.

Of these U.S. Treasury Securities, 95% have been floated since the end of World War II to finance the Cold War against the "Evil Empire." Now Communism has been deflated as an enemy; nativist fascist movements are being pumped up all around the globe and the aggregate Debt is approaching the net worth of all the real estate and movables on the planet. Now, also, the U.S. and Russia are joining their military and space programs, the U.S. is becoming by degrees a full-blown totalitarian state, and the bankers are beginning to foreclose upon the bankrupted minions and dupes within their new global condominium.

The Bank for International Settlements (BIS), the "first beast", was founded in 1930 and was the first entity to be called a "World Bank." Monetarist and gold-based, it functions as a clearing house for the balance of payments between nations. It operated throughout WWII as an interlocking directorate and a clearinghouse for joint Allied and Axis high finance.

The World Bank/International Monetary Fund (IMF), the "Second Beast," was founded in 1946, after being drafted at Bretton Woods, New Hampshire, during the war in 1944. The IMF functions as the collection agency for the World Bank, much as the IRS functions as the collection agency for the Federal Reserve Bank. The Wall Street branch of the Federal Reserve is the "fiscal agent" for the IMF in the USA. The capital pool of the IMF consists of the Prime Banks of the First World, which interlock with the First World (G-7) military-industrial complexes and the oil conglomerates.

The IMF functions under the aegis of the United Nations, as a Keynesian paper credit-mill, extending credit in the form of Special Drawing Rights (SDRs) to the Second and Third World debtor nations, requiring that they purchase specified amounts of the currency of the G-7 nations, imposing "austerity terms" upon their internal economies, and looting them by means of "repayment schedules" of their natural resources and minerals. These are channeled through the General Agreement on Tariffs and Trade (GATT) to the multinational cartels, also headquartered in Geneva, Switzerland.

With the implementation of NAFTA and the Uruguay Round of GATT, the real wages of blue and white collar workers in the U.S. will be leveled in time to near parity with the Third World. The last "Superpower," the United States, is not the primary head of the G-7 Beast, but is, owing to its debtor status, the last head, appropriately close to the horned tail, engaging disproportionately in UN Security Council "police actions" around the globe.

International Capital, having gone "global," will increasingly employ the blue-helmeted troops of the UN to enforce the hegemony of Capital in the future.

Mark Evans

North Coast HOME

Electrons to the Editor

BIS

- Board and Senior Officials - July 2001

BIS

- Board and Senior Officials - July 2001

Urban Bäckström, Stockholm (Chairman of the Board of Directors, President of the Bank)

Lord Kingsdown, London (Vice-Chairman)

Vincenzo Desario, Rome;

David Dodge, Ottawa;

Antonio Fazio, Rome;

Sir Edward A J George, London;

Alan Greenspan, Washington;

Hervé Hannoun, Paris;

Masaru Hayami, Tokyo;

William J McDonough, New York;

Guy Quaden, Brussels;

Jean-Pierre Roth, Zürich;

Hans Tietmeyer, Frankfurt am Main;

Jean-Claude Trichet, Paris;

Alfons Vicomte Verplaetse, Brussels;

Nout H E M Wellink, Amsterdam;

Ernst Welteke, Frankfurt am Main

Bruno Bianchi or Stefano Lo Faso, Rome;

Roger W Ferguson or Karen H Johnson, Washington;

Jean-Pierre Patat or Marc-Olivier Strauss-Kahn, Paris;

Ian Plenderleith or Clifford Smout, London;

Peter Praet or Jan Smets, Brussels;

Jürgen Stark or Stefan Schönberg, Frankfurt am Main

Andrew Crockett, General Manager

André Icard, Deputy General Manager

Gunter D Baer, Secretary General, Head of Department

William R White, Economic Adviser, Head of Monetary and Economic Department

Robert D Sleeper, Head of Banking Department

Renato Filosa, Manager, Monetary and Economic Department

Mario Giovanoli, General Counsel, Manager

Günter Pleines, Deputy Head of Banking Department

Peter Dittus, Deputy Secretary General

Josef ToÆovský, Chairman, Financial Stability Institute

George Pickering, Chief Representative

Carlo Azeglio Caiampi - Italian politician

Lamberto Dini - Italian politician and banker - board of directors BIS

Antonino Occhiuto Italian central banker - BIS 1975 - now

Tommaso Padoa-Schioppa - Italian central banker - BIS 1993 - now

On a bright May morning in 1944, while young Americans were dying on the Italian beachheads, Thomas Harrington McKittrick, American president of the Nazi-controlled Bank for International Settlements in Basle, Switzerland, arrived at his office to preside over a fourth annual meeting in time of war. This polished American gentleman sat down with his German, Japanese, Italian, British, and American executive staff to discuss such important matters as the $378 million in gold that had been sent to the Bank by the Nazi government after Pearl Harbor for use by its leaders after the war. Gold that had been looted from the national banks of Austria, Holland, Belgium, and Czechoslovakia, or melted down from the Reichsbank holding of the teeth fillings, spectacle frames, cigarette cases and lighters, and wedding rings of the murdered Jews.

The Bank for International Settlements was a joint creation in 1930 of the world's central banks, including the Federal Reserve Bank of New York. Its existence was inspired by Hjalmar Horace Greeley Schacht, Nazi Minister of Economics and president of the Reichsbank, part of whose early upbringing was in Brooklyn, and who had powerful Wall Street connections. He was seconded by the all important banker Emil Puhl, who continued under the regime of Schacht's successor, Dr. Walther Funk.

Sensing Adolf Hitler's lust for war and conquest, Schacht, even before Hitler rose to power in the Reichstag, pushed for an institution that would retain channels of communication and collusion between the world's financial leaders even in the event of an international conflict. It was written into the Bank's charter, concurred in by the respective governments, that the BIS should be immune from seizure, closure or censure, whether or not its owners were at war. These owners included the Morgan-affiliated First National Bank of New York (among whose directors were Harold S. Vanderbilt and Wendell Willkie), the Bank of England, the Reichsbank, the Bank of Italy, the Bank of France, and other central banks. Established under the Morgan banker Owen D. Young's so-called Young Plan, the BIS's ostensible purpose was to provide the Allies with reparations to be paid by Germany for World War I. The Bank soon turned out to be the instrument of an opposite function. It was to be a money funnel for American and British funds to flow into Hitler's coffers and to help Hitler build up his machine.

The BIS was completely under Hitler's control by the outbreak of World War II. Among the directors under Thomas H. McKittrick were Hermann Shmitz, head of the colossal Nazi industrial trust I.G. Farben, Baron Kurt von Schroder, head of the J.H. Stein Bank of Cologne and a leading officer and financier of the Gestapo; Dr. Walther Funk of the Reichsbank, and, of course, Emil Puhl. These last two figures were Hitler's personal appointees to the board.

The BIS's first president was the smooth old Rockefeller banker, Gates W. McGarrah, formerly of the Chase National Bank and the Federal Reserve Bank, who retired in 1933. His successor was the forty-three-year-old Leon Fraser, a colorful former newspaper reporter on the muckraking NewYork World, a street-corner soapbox orator, straw-hat company director, and performer in drag in stage comedies. Fraser had little or no background in finance or economics, but he had numerous contacts in high business circles and a passionate dedication to the world of money that acknowledged no loyalties or frontiers. In the first two years of Hitler's assumption of power, Fraser was influential in financing the Nazis through the BIS. When he took over the position of president of the First National Bank at its Manhattan headquarters in 1935, he continued to exercise a subtle influence over the BIS's activities that continued until the 1940s.

Other directors of the Bank added to the powerful financial group. Vincenzo Azzolini was the accomplished governor of the Bank of Italy. Yves Breart de Boisanger was the ruthlessly ambitious governor of the Bank of France; Alexandre Galopin of the Belgian banking fraternity was to be murdered in 1944 by the Underground as a Nazi collaborator.

The BIS became a bête noire of U.S. Secretary of the Treasury Henry Morgenthau, a deliberate, thorough, slow-speaking Jewish farmer who, despite, his origins of wealth, mistrusted big money and power. A model of integrity obsessed with work, Morgenthau considered it his duty to expose corruption wherever he found it. Tall and a trifle ungainly, with a balding high-domed head, a high-pitched, intense voice, small, probing eyes, pince-nez, and a nervous, hesitant smile, Morgenthau was the son of Woodrow Wilson's ambassador to Turkey in World War I. He learned early in life that the land was his answer to the quest for a decent life in a corrupt society. He became obsessed with farming and, at the age of twenty-two, in 1913, borrowed money form his father to buy a thousand acres at East Fishkill, Dutchess County, New York, in the Hudson Valley, where he became Franklin D. Rossevelt's neighbor. During World War I he and Roosevelt formed an intimate friendship. Elinor Morgenthau became very close to her near namesake, Eleanor Roosevelt. While Roosevelt soared in the political stratosphere, Morgenthau remained rooted in his property. In the early 1920s he published a newspaper called The American Agriculturist that pushed for government credits for farmers. When Roosevelt became governor of New York in 1928, he appointed Morgenthau chairman of the Agricultural Advisory Commission. Morgenthau showed great flair and a passionate commitment to the cause of the sharecropper.

Legend has it that on a freezing winter day in 1933, FDR and Morgenthau met and talked on the borderline of their two farms. Morgenthau is supposed to have said to Roosevelt, "Life is getting slow around here". And FDR replied, "Henry, how would you like to be Secretary of the Treasury?"

What he lacked in knowledge of economics, Morgenthau rapidly made up in his Jeffersonian principles and role as keeper of the public conscience. Close to a thousand volumes of his official diaries in the Roosevelt Memorial Library at Hyde Park give a vivid portrait of his inspired conducting of his high office. He was aided by an able staff, which he ran with benign but military precision. His most trusted aide was his Assistant Secretary, Harry Dexter White. Unlike Morgenthau, White came form humble origins. Jewish also, he was the child of penniless Russian immigrant parents who were consumed with a hatred of the czarist regime. White's early life was a struggle: this short, energetic, keen-faced man fought to help his father's hardware business succeed, finally forging as an economist with the aid of a Harvard scholarship and a professorship at Lawrence College, Wisconsin. He was opinionated and self-confident to a degree. Although he was frequently accused of being a communist sympathizer, he was in fact simply an old-fashioned liberal driven by his ancestral memories of Russian imperialism.

It is unfortunate that Morgenthau did not appoint White as his representative at BIS meetings, but White was too valuable in Washington. Instead, Morgenthau sent the more questionable Merle Cochran to investigate the BIS. Cochran was on loan to Treasury from the State Department; he represented the State Department's sophisticated neutralism before (and during) the war. Cochran became Secretary of the American Embassy in Paris, working directly under Roosevelt's friend the duplicitous, Talleyrand-like Ambassador William Bullitt. Cochran spent most of his time in Basle conveying to both Morgenthau and Cordell Hull details of what the BIS was up. Very much opposed to White- indeed, violently so- Cochran was sympathetic with the BIS and to the Nazis, as his various memoranda made clear. Morgenthau took Cochran's political judgements with a degree of skepticism, but continued to use him over White's objections because he knew the Germans would trust Cochran and confide much in him. Day after day, Cochran lunched with Schmitz, Shroder, Funk, Emil Puhl, and the other Germans on the BIS board, obtaining a clear picture of the BIS's plans for the future.

In March 1938, when the Nazis marched into Vienna, much of the gold of Austria was looted and packed into vaults controlled by the Bank for International Settlements. The Nazi board members forbade any discussion of the transaction at the BIS summit meetings in Basle. Cochran, in his memoranda to Morgenthau, failed to score this outrageous act of theft. The gold flowed into the Reichsbank under Funk, in the special charge of Reichsbank vice-president and BIS director, Emil Puhl. On March 14, 1939, Cochran wrote to Morgenthau, "I have known Puhl for several years, and he is a veteran and efficient officer." He also praised Walther Funk.

His timing was not good. One day later, Hitler followed his forces into Prague. The storm troops arrested the directors of the Czech National Bank and held them gunpoint, demanding that they yield up $48 million gold reserve that represented the national treasure nounced that they had already shifted the gold to the BIS with instructions that it be forwarded to the Bank of England. This was an act of great naiveté. Montagu Norma, the eccentric, Vandykebearded governor of the Bank of England, who liked to travel the world disguised as Professor Skinner in a black opera cloak, was a rabid supporter of Hitler.

On orders from their German captors, the Czech directors asked the Dutch BIS president, J.W. Beyen, to return the gold to Basle. Beyen held an anxious discussion with BIS general manager Roger Auboin of the Bank of France. The result was that Beyen called London and instructed Norman to return the gold. Norman instantly obliged. The gold flowed into Berlin for use in buying essential strategic materials toward a future war.

There the matter might have been buried had it not been for a young , very bright, and idealistic London journalist and economist named Paul Einzig, who had been tipped off to the transaction by a contact at the Bank of England. He published the story in the Financial News. The story caused a sensation in London. Einzig held a hasty meeting with maverick Labour Member of Parliament George Strauss. Strauss through Einzing began investigating the matter.

Henry Morgenthau telephoned Sir John Simon, British Chancellor of the Exchequer, on a Sunday night in an effort to determine what was going on. Merle Cochran had telegraphed him with a characteristic whitewash of the BIS and an outright dismissal of Einzig's charges that the BIS was a Nazi outfit. Sir John said icily on the transatlantic wire, "I'm in the country, Mr. Secretary. We are enjoying our dinner. It is not our custom to do business by telephone."

"Well, Sir John," Morgenthau replied, "we've been doing business by telephone over here for almost forty year!"

Sir John Simon continued to dodge Morgenthau's questions. On May 15, George Strauss asked Prime Minister Neville Chamberlain, "It is true, sir, that the nation treasure of Czechoslovakia is being given to Germany?" "It is not," the Prime Minister replied. Chamberlain was a major shareholder in Imperial Chemical Industries, partner of I.G. Farben whose Hermann Shcmitz was on the board of the BIS. Chamberlain's reply threw the Commons into an uproar Einzig refused to let go. He was convinced that Norman had transferred the money illegally in collusion with Sir John Simon. Simon, in answer to a question from Strauss, denied any knowledge of the matter.

Next day, Einzing tackled Sir Henry Strakosch, a prominent political figure. Strakosch refused to disclose the details of the conversation he had had with Simon. But Strakosch finally cracked and admitted that Simon had discussed the transfer of the Czech gold.

Einzig was jubilant. He called Strauss with the news. Strauss put a further question to Sir John Simon in a debate on May 26. Once again, Simon hedged. Winston Churchill was the leader of a violent onslaught on the unfortunate Chancellor of the Exchequer.

Morgenthau demanded to know more. Cochran's letter from Basle dated May 9 and received May 17 brushed over the issue once more. Cochran wrote,

There is an entirely cordial atmosphere at Basle; most of the central bankers have known each other for many years, and these reunions are enjoyable as well as profitable to them. I have had talks with all of them. The wish was expressed by some of them that their respective statesmen might quit hurling invectives at each other, get together on a fishing trip with President Roosevelt or to the World's Fair, overcome their various prides and complexes, and enter into a mood that would make comparatively simple the solution of many of the present political problems.

This picture of good cheer scarcely convinced Morgenthau. On May 31, Associated Press reported from Switzerland that transactions were completed between the BIS and the Bank of England and the Czech gold was now firmly in Berlin.

During World War II, Einzig, who had never forgotten the Czech gold affair, ran into J.W. Beyen in London and asked him if he would now admit what had taken place. Beyen said smoothly, "It is all technical. The gold never left London." Einzig was amazed. He wrote an apology to Beyen in his book of memoirs, In the Center of the Things.

The truth was that the gold had not had to leave London in order to be available in Berlin. The arrangement between the BIS an its member banks was that transactions were not normally made by shipments would show up counts. Thus, all Montagu Norman had to do was to authorize Beven and replace the same amount from the Czech National Bank holdings in London.

By 1939, the BIS had invested millions in Germany, while Kurt von Schroder and Emil Puhl deposited large sums in looted gold in the Bank. The BIS was an instrument of Hitler, but its continuing existence was approved by Great Britain even after that country went to war with Germany, and the British director Sir Otto Niemeyer, and chairman Montagu Norman, remained in office throughout the war.

In the middle of the Czech gold controversy, Thomas Harrington McKittrick was appointed president of the Bank, with Emil Meyer of the Swiss National Bank as chairman. White-haired, pink-cheeked, smooth and soft-spoken, McKittrick was a perfect front man for The Fraternity, an associate of the Morgans and an able member of the Wall Street establishment. Born in St. Louis, he went to Harvard, where he edited the Crimson, graduating as bachelor of arts in 1911. He worked his way up to become chairman of the British-American Chamber of Commerce, which numbered among its members several Nazi sympathizers. He was a director of Lee, Higginson and Co., and made substantial loans to Germany. He was fluent in German, French and Italian. Though he spent all of his career inland, he wrote learned papers on the life and habits of seabirds. His wife, Marjorie, and his four pretty daughters, one of whom was at Vassar and a liberal enemy of the BIS, were popular on both sides of the Atlantic.

Early in 1940, McKittrick traveled to Berlin and held a meeting at the Reichsbank with Kurt von Schröder of the BIS and the Gestapo. They discussed doing business with each other's countries if war between them should come.